Implications of the Capital Gains Increase in Canada for Personal Donations

Canada's recent increase in the capital gains inclusion rate, effective June 25, 2024, has stirred significant discussion among investors, philanthropists, and financial professionals. As the government aims to bolster public revenue, the ripple effects of this policy change are multifaceted, particularly when it comes to charitable donations. This article delves into the implications of the capital gains increase on donations, exploring both the challenges and opportunities that arise for personal donors and charitable organizations. In September’s article, we’ll focus more on the impact and additional incentive to donate using either operating or holding company donations.

Understanding Capital Gains Tax and the Inclusion Rate

Capital gains tax is levied on the profit realized from the sale of an asset. The inclusion rate determines the portion of the capital gain that is subject to taxation. Until recently, Canada taxed only 50% of the capital gain. With the new policy effective June 25, 2024, personal capital gains remain taxed at 50% up to $250,000, but any gains above this threshold are taxed at 67%. Corporate capital gains, on the other hand, are taxed at the 67% rate regardless of the amount.

Impact on Personal Investors

For personal investors, especially those with significant capital gains exceeding $250,000, the increase in the inclusion rate has substantial financial implications. For instance, an investor with $1,000,000 in capital gains would previously report 50% or $500,000 as taxable income. Under the new inclusion rate, the first $250,000 of gains is taxed at 50% ($125,000 taxable), and the remaining $750,000 is taxed at 67% ($502,500 taxable), making the total taxable amount $627,500. That results in an extra $61,200 of tax payable at Alberta’s highest marginal tax rate.

At first glance, this additional tax burden may discourage investors from triggering gains, affecting their investment strategies and liquidity. However, by donating appreciated assets directly to charities, rather than triggering gains and donating cash, these investors can avoid the higher capital gains tax while supporting causes they care about. This approach allows them to maximize their tax deductions and make a more significant impact with their contributions by eliminating the tax grind on after-tax donations.

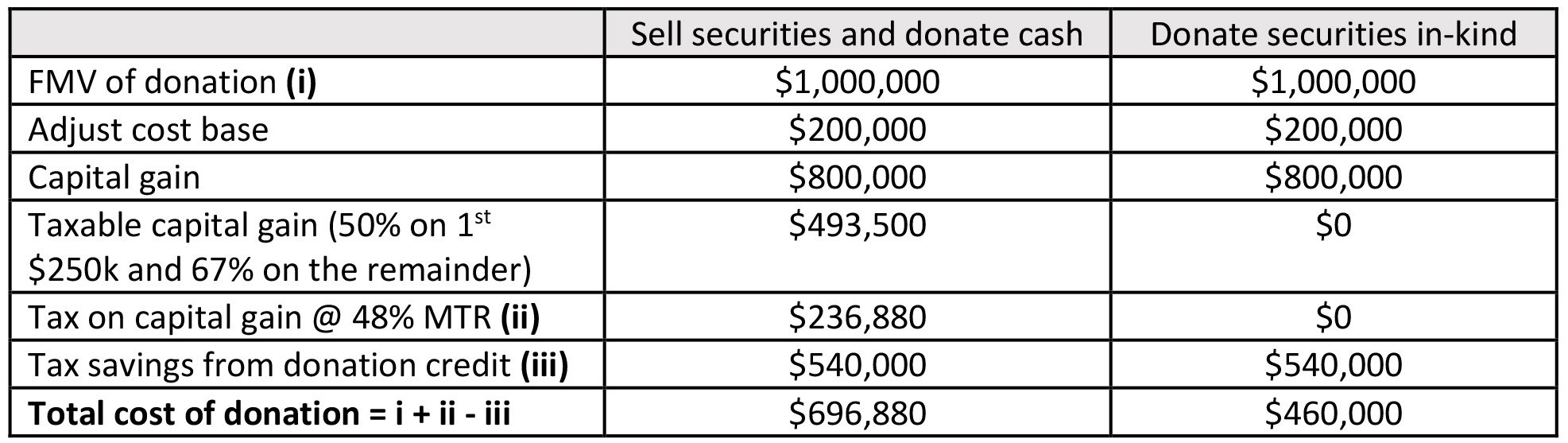

Comparison of donating cash or securities to Unison Alberta:

As a result of donating appreciated investments and eliminating the capital gains tax, this individual had tax savings of $236,880 rather than selling the investments and donating with after-tax cash.

Strategic Donations: The Silver Lining

Despite the higher capital gains inclusion rate, there remains a silver lining for donors. The incentive to donate appreciated securities directly to charities is more appealing than ever. By doing so, donors can bypass the increased capital gains tax, allowing them to give more generously. This strategy not only benefits the donors by reducing their taxable income but also ensures that charities receive more substantial support. It’s important to note that donations like this can trigger alternative minimum tax (AMT) and should be explored first with your financial professionals.

Reach out to your financial professional or contact me with further questions.